Make success possible with our Latest and Unique CIMA Advanced Diploma In Management Accounting P2 Practice Exam!

Name: Advanced Management Accounting

Exam Code: P2

Certification: CIMA Advanced Diploma In Management Accounting

Vendor: CIMA

Total Questions: 202

Last Updated: October 10, 2025

341 Satisfied Customers

Success is simply the result of the efforts you put into the preparation. We at Dumpsgroup wish to make that preparation a lot easier. The Advanced Management Accounting P2 Practice Exam we offer is solely for best results. Our IT experts put in their blood and sweat into carefully selecting and compiling these unique Practice Questions. So, you can achieve your dreams of becoming a CIMA Advanced Diploma In Management Accounting professional. Now is the time to press that big buy button and take the first step to a better and brighter future.

Passing the CIMA P2 exam is simpler if you have globally valid resources and Dumpsgroup provides you just that. Millions of customers come to us daily, leaving the platform happy and satisfied. Because we aim to provide you with CIMA Advanced Diploma In Management Accounting Practice Questions aligned with the latest patterns of the Advanced Management Accounting Exam. And not just that, our reliable customer services are 24 hours at your beck and call to support you in every way necessary. Order now to see the P2 Exam results you always desired.

You must have heard about candidates failing in a large quantity and perhaps tried yourself and fail to pass Advanced Management Accounting. It is best to try Dumpsgroup’s P2 Practice Questions this time around. Dumpsgroup not only provides an authentic, valid, and accurate resource for your preparation. They simplified the training by dividing it into two different formats for ease and comfort. Now you can get the CIMA P2 in both PDF and Online Test Engine formats. Choose whichever or both to start your CIMA Advanced Diploma In Management Accounting certification exam preparation.

Furthermore, Dumpsgroup gives a hefty percentage off on these Spoto P2 Practice Exam by applying a simple discount code; when the actual price is already so cheap. The updates for the first three months, from the date of your purchase, are FREE. Our esteemed customers cannot stop singing praises of our CIMA P2 Practice Questions. That is because we offer only the questions with the highest possibility of appearing in the actual exam. Download the free demo and see for yourself.

We know you have been struggling to compete with your colleagues in your workplace. That is why we provide the P2 Practice Questions to let you gain the upper hand that you always wanted. These questions and answers are a thorough guide in a simple and exam-like format! That makes understanding and excelling in your field way lot easier. Our aim is not just to help to pass the CIMA Advanced Diploma In Management Accounting Exam but to make a CIMA professional out of you. For that purpose, our P2 Practice Exams are the best choice.

There are many resources available online for the preparation of the Advanced Management Accounting Exam. But that does mean that all of them are reliable. When your future as a CIMA Advanced Diploma In Management Accounting certified is at risk, you have got to think twice while choosing CIMA P2 Practice Questions. Dumpsgroup is not only a verified source of training material but has been in this business for years. In those years, we researched on P2 Practice Exam and came up with the best solution. So, you can trust that we know what we are doing. Moreover, we have joined hands with CIMA experts and professionals who are exceptional in their skills. And these experts approved our P2 Practice Questions for Advanced Management Accounting preparation.

A company has a 31 December year end and pays corporation tax at a rate of 30%. Corporation tax is payable 12 months after the end of the year to which the cash flows relate. The company can claim tax allowable depreciation at a rate of 25% reducing balance. It pays $1 million for a machine on 31 December 20X4. The company's cost of capital is 10%. What is the present value of the benefit of the first portion of tax allowable depreciation?

A. $250,000

B. $227,500

C. $75,000

D. $68,175

ANSWER : D

Which TWO of the following expressions are correct?

A. 1 + money rate = (1 + real rate) x (1 + inflation rate)

B. 1 + real rate = (1 + money rate) / (1 + inflation rate)

C. 1 + real rate = (1 + inflation rate) / (1 + money rate)

D. 1 + money rate = (1 + inflation rate) / (1 + real rate)

E. 1 + inflation rate = (1 + money rate) x (1 + real rate)

ANSWER : A,B

Which TWO of the following are reasons why cost-based approaches to transfer pricing are often used in practice?

A. The buying division will want to maximize its profits.

B. The transferring division will want to maximize its profits.

C. Because the external market is imperfect.

D. Because there is often no external market for the product that is being transferred.

E. The approach allows the organization to cover all the costs.

ANSWER : C,D

If transfer prices are set at variable costs, the supplying division does not cover its fixed costs.

Which of the following does NOT resolve this problem?

A. Each division can be given a share of the overall contribution earned by the organization.

B. A system of dual pricing can be adopted.

C. Reduce the level of fixed costs.

D. Central management can impose a range within which the transfer price should fall.

ANSWER : C

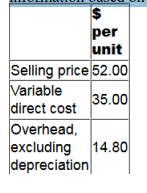

A company is considering investing $680,000 in a machine to manufacture a new product. A

consultant has been appointed to advise on the investment and the company is committed to

paying $10,000 to the consultant in year 1, even if the project does not go ahead.

300,000 units of the new product will be produced and sold each year. Unit cost and revenue

information based on this level of output is as follows.

60% of the overhead cost is variable. Of the remainder, 10% consists of allocated head office

overheads.

The selling price will increase by 2% each year in line with inflation, beginning in year 2. Fixed

price contracts mean that all unit costs will remain unaltered.

Taxation information:

• 100% first year allowance will be available for the purchase of the machinery.

• The taxation rate is 30% of taxable profits, payable in the year after that in which the liability

arises.

For the purpose of deciding whether to proceed with the investment, what is the relevant cash

flow in year 2?

A. $1,102,320

B. $1,099,320

C. $1,326,960

D. $1,288,800

ANSWER : A

A company currently absorbs production overheads based on labor hours. The overheads

absorbed by the two products that are made, L and M, are $4 per unit and $10 per unit

respectively. These were based on the budgeted overheads of $7,000 and budgeted labor hours of

1,750. The budgeted output was 500 units of each product.

The company is investigating the use of activity based costing (ABC). Analysis has shown that

the total production overheads of $7,000 are made up of $4,000 for set up costs and $3,000 for

inspection costs. The cost driver for set up costs is the number of set ups and for inspection costs

it is the number of inspections.

The cost driver rate for set ups is $160 per set up. Product L would need 5 production runs. Both

types of product would need 1 set up for each production run.

Product L would need 2 inspections for each production run. Product M would need 1 inspection

per production run.

The products are made in the same department and use the same equipment and staff but they are

produced separately.

Which of the following statements are correct?

Select ALL that apply.

A. The current production overhead absorption rate is $4.00 per hour.

B. The current production overhead absorption rate is $500 per hour.

C. If ABC was used, set up costs per unit of Product L would be $1.60.

D. If ABC was used, set up costs per unit of Product M would be $4.00.

E. If ABC was used, inspection costs per unit of Product L would be $4.00.

F. If ABC was used, inspection costs per unit of Product M would be $4.00.

ANSWER : A,C,F

Dumpsgroup is a verified platform for certification preparation. Our expert professionals are working day and night to create the perfect Practice Exam so you can pass your exam with flying colors. We provide only the authentic and valid Practice Questions approved by IT Experts. Start your certification journey now!

www.dumpsgroup.com

support@dumpsgroup.com

1104 Long Street, NY, 11206, USA

Feel free to contact us, we are available 24/7.